Hurricane Travel Insurance: Coverage, Expert Tips, and When to Buy

June 9, 2025 - Skylar

Last Updated On:

Coastal destinations are some of the most popular vacation spots for many reasons. Warm beaches. Surfing. The smell of fresh, salty air. However, there’s one looming risk of planning a vacation next to the ocean: hurricanes. Are you traveling to a hurricane-prone area, especially during hurricane season? Then here’s what you need to know about hurricane travel insurance and how you best prepare for a safe trip–no matter what might happen.

Quick Answer: Does Travel Insurance Cover Hurricanes?

Hurricane travel insurance can reimburse your prepaid, non-refundable trip costs if a storm disrupts your plans, but only when specific conditions are met. Most standard policies cover cancellations or interruptions if a named hurricane causes your destination to become uninhabitable, shuts down travel services for 12–48 hours, or triggers a mandatory evacuation order.

However, timing is critical. If the storm is already named before you purchase your policy, it’s usually considered a foreseeable event and won’t be covered. For broader flexibility, like canceling due to uncertainty before a storm escalates, you’ll need Cancel For Any Reason (CFAR) coverage, which typically reimburses 50–75% of your trip cost.

Key Takeaways

Coverage depends on when you buy because named storms before purchase usually aren’t covered.

Claims are triggered by specific events like evacuations, closures, or travel shutdowns.

Standard plans reimburse up to 100%, while CFAR offers flexibility at a 50–75% reimbursement.

The best strategy is to buy early and choose coverage based on your risk tolerance.

Hurricanes, typhoons, and cyclones are different names for the same weather phenomenon. It’s a tropical storm with violent winds and thunderstorms. A hurricane begins over the ocean and can cause astronomical damage when it reaches shore, such as flooding. The name for this tropical storm will differ depending on where you are in the world. So here’s a quick breakdown for you:

Hurricanes: Atlantic Ocean and Northeast Pacific Ocean

Typhoons: Northwest Pacific Ocean

Cyclones: South Pacific Ocean and Indian Ocean

Additionally, “hurricane season” differs depending on your location in the world. Here’s when you’re most likely to experience a hurricane, typhoon, or cyclone.

Hurricanes: June to November

Typhoons: April to December

Cyclones: November to April

Thankfully, we have such advanced technology to track tropical storms, so you are unlikely to get caught in a hurricane without notice. Even so, you can travel to a hurricane-prone region with peace of mind by taking these extra measures before leaving.

Is A Hurricane Covered Under Travel Insurance?

Yes. Most comprehensive travel insurance policies will cover natural disasters like hurricanes. However, you cannot get a travel insurance policy after a hurricane is “named”. This is because a named storm is no longer an “unforeseen circumstance.” That’s why it’s important to purchase hurricane travel insurance as soon as possible after booking your trip, especially if you’re traveling to a hurricane-prone region when hurricanes are most likely to happen.

Travel Insurance Benefits That Protect You During a Hurricane

When a hurricane disrupts your travel plans, it makes the biggest difference to have the right travel insurance. Here’s a breakdown of essential travel insurance benefits that can help you manage unexpected costs and challenges caused by severe weather events like hurricanes.

Trip Cancellation

If a hurricane forces you to cancel your trip before departure, trip cancellation coverage reimburses you for non-refundable prepaid expenses such as flights, hotels, and tours. This benefit typically applies when the hurricane is officially named after you purchase your policy and affects your destination or departure point, allowing you to recover your trip investment without financial loss. Learn how other natural disasters trigger trip cancellation coverage.

Trip Interruption

In cases where a hurricane cuts your trip short or forces you to return home early, trip interruption coverage reimburses the unused portion of your trip and additional return flight costs to get you home safely. This benefit helps provide coverage for last-minute flights. That way, you’re not left stranded or forking out extra costs due to sudden changes.

Medical Expense Coverage

Hurricanes can lead to injuries or illnesses, especially during evacuations or storm-related accidents. Medical expense coverage pays for emergency medical treatment, hospital stays, surgeries, and prescriptions incurred while traveling. If local healthcare facilities are overwhelmed, medical evacuation coverage could also assist in transporting you to a facility that can better treat you.

Travel Delay

Hurricanes often cause flight cancellations and long delays. Travel delay coverage reimburses expenses such as meals, accommodations, and local transportation if your trip is delayed for a specified number of hours due to a hurricane. This benefit helps cover unexpected costs while you wait out the storm or reschedule your travel.

Missed Connection

If a hurricane disrupts your connecting flights, causing you to miss a scheduled connection, missed connection coverage reimburses additional transportation or lodging expenses incurred to catch up with your original itinerary. This ensures that weather-related disruptions don’t derail your entire travel plan. We’ve written an entire article on missed connection insurance, so check it out if you’re interested in learning more.

How Hurricane Travel Insurance Actually Works (Beyond the Basics)

Understanding hurricane travel insurance comes down to one concept: what triggers coverage and when.

What Standard Policies Typically Cover

Most comprehensive travel insurance plans (including options from AXA, IMG, and Travel Insured International) include trip cancellation and interruption benefits that may apply when:

A named hurricane makes your destination uninhabitable

Your common carrier (flight/cruise) is cancelled due to the storm

Your hotel or resort is uninhabitable or severely damaged

Local authorities issue a mandatory evacuation order

Trip cancellation overage typically reimburses 100% of prepaid, non-refundable trip costs if the event meets policy criteria.

The “Named Storm” Rule (Critical Timing Factor)

Travel insurance is built around unforeseen events.

If a storm is already named by the National Hurricane Center before you purchase your policy:

It is considered a foreseeable event

Claims related to that storm are typically excluded

This is one of the biggest reasons claims get denied.

Pro Tip: You’ll likely need Cancel For Any Reason (CFAR) to cover these concerns since they’re not usually covered under standard trip cancellation benefits.

When CFAR Becomes Necessary

CFAR is the ultimate flexibility upgrade option for hurricane season.

It allows you to cancel:

Before a storm becomes severe

Without needing an official trigger

For personal risk tolerance reasons

Tradeoffs:

Reimburses 50–75% of trip cost (not 100%)

Must be purchased early (usually within 1–21 days of deposit)

Hurricane coverage isn’t about whether a storm exists. Instead, it’s about:

When it was named

What official actions occurred

How your policy defines a “covered event”

Is Your Hurricane Situation Likely Covered?

To give you an actionable idea if hurricane travel insurance applies to a possible situation you might experience during your trip, check out the table below.

Situation

Typically Covered?

Your resort becomes uninhabitable due to a named hurricane

Often yes

A mandatory evacuation order is issued

Often yes

Your flight is cancelled due to a named storm

Often yes

You purchased insurance after the storm was named

Usually no

You decide not to travel because you’re worried about the forecast

Usually no

You cancel because of uncertainty before a storm arrives

Usually only with CFAR

These are just examples, so be sure to always read the policy language for the plan you’re considering purchasing.

Yonder Expert Tip:

The “clock” starts the moment the National Hurricane Center (NHC) or World Meteorological Organization (WMO) assigns a name. Even if the storm is 1,000 miles away and “just a tropical storm,” once it has a name, it is a foreseeable event.

Hurricane Travel Insurance Comparison: What Different Plans Actually Cover

This table compares how the top plans available through Yonder Travel Insurance respond to specific hurricane-related triggers, not just general coverage.

Plan

Trip Cancellation (Hurricane)

Service Cessation (12–48 hrs)

Accommodation Uninhabitable

Mandatory Evacuation (24+ hrs)

Military Duty (Disaster Response)

Trip Interruption

CFAR Available

Typical Price Range

Battleface Discovery

Yes

—

Yes

Yes

—

Yes

No

$–$$

Travel Insured FlexiPAX

Yes

—

Yes

Yes

Yes

Yes

Yes

$$

AXA Gold

Yes

Yes

Yes

—

Yes

Yes

No

$$

AXA Platinum

Yes

Yes

Yes

—

Yes

Yes

Yes

$$–$$$

Aegis Choice

Yes

—

Yes

Yes

Yes

Yes

No

$

IMG Travel Lite

Yes

—

Yes

Yes

Yes

Yes

No

$–$$

IMG Travel SE

Yes

—

Yes

Yes

Yes

Yes

Yes

$$

IMG Travel LX

Yes

—

Yes

Yes

Yes

Yes

Yes

$$$

What These Hurricane Coverage Triggers Actually Mean

Here’s a quick de-coder to better understand the covered reasons defined in the chart above. Please note that these will vary from plan to plan, so don’t forget to review the specific certificate for exact details.

Service Cessation (12–48 hours) Coverage may apply if transportation services (like flights or ferries) are completely shut down for a defined period due to a hurricane.

Accommodation Uninhabitable One of the most common and reliable triggers. If your hotel, resort, or vacation rental is damaged or unsafe, cancellation or interruption benefits typically apply.

Mandatory Evacuation (24+ hours) If local authorities order an evacuation that prevents you from staying at your destination, many plans treat this as a covered event.

Military Duty (Disaster Response) If you’re called to active duty due to a natural disaster response, some plans allow cancellation reimbursement.

Hurricane Risks Travelers Often Overlook

Many travelers assume the biggest hurricane-related risk is canceling a trip before departure. In reality, some of the most common disruptions happen after travel has already begun. Avoid a denied claim by understanding these important areas.

Delays Can Be More Common Than Cancellations

A hurricane doesn’t always force travelers to cancel entirely. More often, it can lead to delayed flights, missed connections, additional hotel nights, or transportation disruptions that create unexpected expenses.

Yonder Expert Tip: Most policies require a “Common Carrier” (airline/cruise line) to be completely shut down for a specific window, usually 12 to 48 consecutive hours, before the “Trip Cancellation” benefit kicks in.

Small Travel Delays Can Create Large Costs

A one-day flight cancellation may not sound significant, but additional lodging, meals, airport transfers, and rebooking expenses can add up quickly, especially for families or groups.

Travelers Often Focus On The Destination And Forget The Departure City

A hurricane doesn’t need to hit your destination directly to affect your trip. Severe weather near your departure airport, connecting airport, cruise embarkation port, or return route can also create covered disruptions.

Yonder Expert Tip: If a hurricane hits your home city and makes your house uninhabitable or the roads to the airport impassable, this is often a covered reason for cancellation, even if the destination is perfectly sunny.

The Biggest Financial Exposure Isn’t Always Airfare

Many travelers focus on flight costs when evaluating risk. However, prepaid resorts, cruises, excursions, tours, and destination wedding expenses often represent a much larger portion of the total trip investment.

“The biggest mistake we see is ‘Forecast Watching.’ Travelers see a storm brewing on the news and wait to buy insurance until they are sure it will hit. In the insurance world, once you’re ‘sure’ it’s coming, it’s already too late to cover it. The best time to buy is the day you book your trip,” explains Boynton.

What Happens If a Hurricane Disrupts Your Trip?(Real Scenarios)

Real-world scenarios are where coverage differences become clear. Check out the scenarios below to better understand how hurricane travel insurance works in real-time.

Scenario 1: Cruise Rerouted Due to Hurricane

Your cruise has to reroute the trip itinerary to avoid a storm. This causes you to miss your tour or excursion on the island the cruise is now avoiding. The tour was nonrefundable, and the tour company won’t offer a refund.

Coverage outcome:

Usually NOT covered under cancellation

May qualify for trip interruption (partial reimbursement of unused trip expenses)

Scenario 2: Resort Closed Before Departure

A hurricane damages a beachfront resort, forcing the property to close temporarily and cancel upcoming reservations.

Coverage outcome:

Typically covered under trip cancellation

Requires proof of closure from supplier or hotel

Scenario 3: Flight Cancelled + Extra Hotel Nights

A hurricane causes widespread flight cancellations, forcing a traveler to stay several extra nights before returning home.

Coverage outcome:

Covered under trip delay/interruption (depending on the plan)

Reimburses meals, lodging, local transport

Scenario 4: Storm Forecast Makes You Nervous

Weather is approaching your destination, but authorities haven’t issued an official storm warning yet. You decide to cancel your trip anyways, just to play it safe.

Coverage outcome:

Only covered if you purchased CFAR

Expert Tips When Filing a Hurricane Travel Insurance Claim

Your bookings are fully refundable, meaning there’s no risk of loss of any trip costs

You’re traveling outside hurricane season

Your financial risk is minimal should something go wrong

Traveler Type

Why Coverage Matters

Cruise travelers

Weather-related itinerary changes & missed ports

Caribbean travelers

Higher storm exposure

Families

Greater rebooking costs

Destination wedding attendees

Significant prepaid expenses

Resort travelers

High non-refundable trip costs

Does Travel Insurance Cover Hurricane Evacuation?

Some policies will include coverage for a non-medical evacuation due to natural disasters. Basically, if the destination country declares a hurricane as an official disaster or the U.S. advises tourists to leave that destination, coverage could apply for a “hurricane evacuation.”

A covered hurricane evacuation would typically transport you to the nearest place of safety or your home, as determined in advance by the sole discretion of the travel insurance company.

“Just make sure you always contact the 24/7 emergency provider included with your policy to coordinate an evacuation, as this is a requirement for coverage,” says Terry Boynton, co-founder and president of Yonder Travel Insurance.

The emergency assistance team will have a better ability to coordinate the evacuation, and in an affordable manner. Usually, the traveler doesn’t pay out of pocket for this when working with the global assistance team. Instead, the travel insurance company would consider it a covered event.

How To Prepare For Travel During Hurricane Season

If you do decide to take a trip to a coastal destination during hurricane season, here are some important steps you can take to keep yourself safe, manage the risk, and still have a good time.

Enroll in STEP

When you enroll in the U.S. Department of State’s Smart Traveler Enrollment Program (STEP), you can opt to receive safety updates on countries you plan to visit, weather-related or not. There are many other helpful resources on this website that can help give you more peace of mind about your future travels.

You can also check the National Hurricane Center website for updates leading up to your trip – they usually name a hurricane 36-48 hours in advance.

Buy Travel Insurance As Soon As Possible

Most comprehensive travel insurance policies include cancellation coverage in the event of a natural disaster, like a hurricane. However, you’ll want to purchase your plan as soon as possible.

“Because once a hurricane is named, it becomes “foreseeable,” and you will no longer be able to purchase a policy with coverage to cancel,” explains Boynton.

Unfortunately, this is one of the most common travel mistakes made by policyholders. But you can guarantee coverage for non-refundable expenses when you purchase your insurance right after you make your first trip deposit.

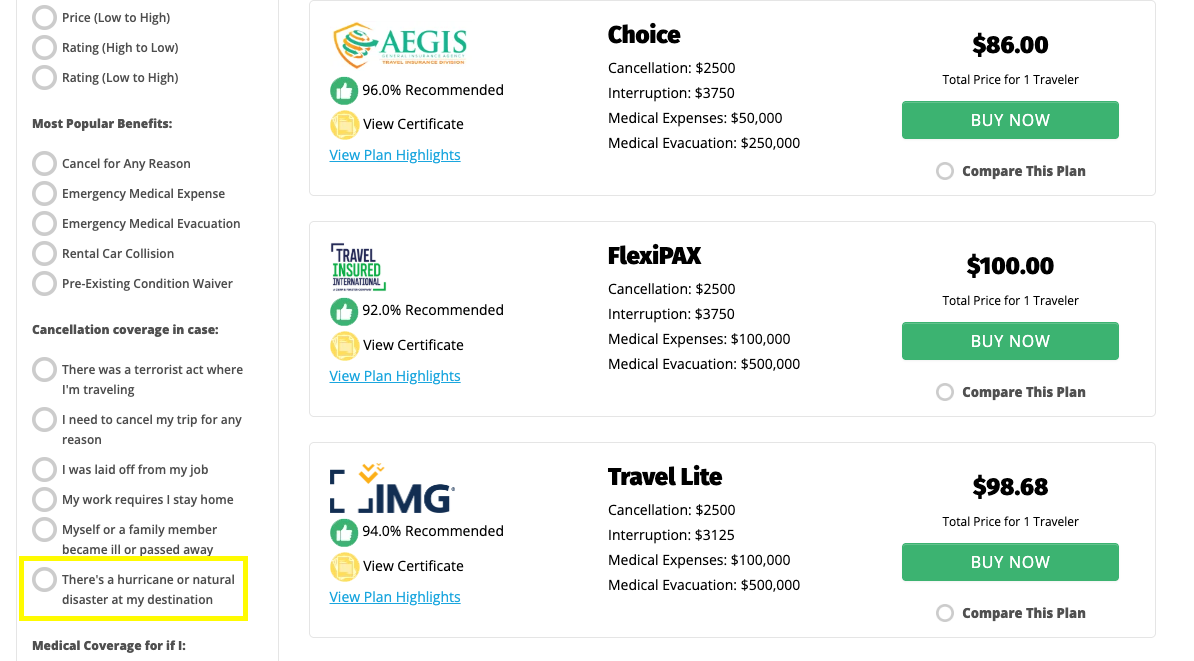

Pro Tip: Are you planning a trip to a hurricane-prone area during hurricane season? Don’t wait until it’s too late. Get a travel insurance quote now! To compare hurricane travel insurance policies with the right coverage for trip cancellation, select the filter for “There’s a hurricane or natural disaster at my.” (See below)

Weather and storms can be unpredictable. Even if the forecast says it will be sunny for your entire trip, you may end up getting caught in the rainy outskirts of a tropical storm. So, make a list of the indoor activities your destination has to offer. From museums to adventure centers to historical sites, you’ll have at least a list of options if you experience an unexpected rainy day.

Determine The Stability Of Your Destination

Strong hurricane winds and high tidal waves can do major damage to infrastructure, so take some time to consider where you are staying. If your condo is along the beach, moving as inland as possible would be a great option. If flooding is a common hazard at your destination, we recommend staying in a low-risk flood zone. Wooden buildings are highly unstable in a hurricane, so you should relocate to a more secure location. Moving to a shelter is your best bet for staying safe.

Plan An Emergency Departure

If the worst-case scenario happens, how hard would it be for you to leave the country? It’s important to check out possible transportation options, especially if you’re traveling outside the United States. Plan an alternative exit route in case an unforeseen storm does happen. It’s better than having no plan at all!

If your vacation is stateside, look at renting a car to drive to a safe zone.

When traveling in a land-locked country, consider buses that route to a safe zone or a safer neighboring country.

If your vacation is happening on an island, this can be a bit more tricky, so your options are limited to boat and plane. Just make sure you check the schedules because the routes fill up fast when there’s a storm about to hit.

Pack Like A Hurricane Might Happen

Even if your trip is right around the corner and the weather looks like it’s going to hold, make sure you’re still prepared with what you pack. Pack a small first aid kit, battery-powered flashlight, and non-perishable foods just in case a natural disaster heads your way.

Since ATMs might not be accessible during and after the storm, we recommend you carry enough cash for yourself and family for two weeks. Again, the likelihood you’ll need to use this storm kit is slim, but it’s worth it to have it on hand, just in case.

Frequently Asked Questions About Hurricane Travel Insurance

Does travel insurance cover cancellations due to hurricanes?

Yes, many comprehensive travel insurance policies include trip cancellation coverage if a hurricane forces you to cancel your trip before departure. However, coverage typically applies only if the hurricane is named after you purchase the policy, so it’s important to buy insurance early.

Can I purchase hurricane travel insurance if a storm has already been forecasted?

Travel insurance policies require you to buy coverage before a hurricane is officially named. Purchasing insurance after a storm is announced usually excludes hurricane-related claims, so it’s important to secure your policy soon after booking your trip.

How can I find affordable travel insurance that covers hurricane-related trip cancellations?

The best way is to compare multiple policies side by side instead of buying from a single provider. Look for plans that include trip cancellation for natural disasters and meet key triggers (like accommodation damage or evacuation orders). Most policies cost 4–10% of your trip, but comparing options helps you find stronger coverage at a similar price.

What should I look for in travel insurance to protect against hurricane disruptions?

Focus on specific coverage “natural disaster” triggers in the policy language under the trip cancellation section. Look for policies that include trip cancellation, trip interruption, and delay benefits tied to events like accommodation becoming uninhabitable, mandatory evacuations, or service shutdowns. If you want flexibility before a storm escalates, consider adding Cancel For Any Reason (CFAR).

Can travel insurance help recover costs if a hurricane forces me to cancel or delay my trip?

Yes, but only if the situation meets your policy’s covered reasons. You may be reimbursed for prepaid, non-refundable costs if a hurricane damages your destination, halts travel services, or causes an evacuation. For delays, coverage can also reimburse meals, lodging, and transportation expenses during disruptions.

Are you feeling more prepared to book your vacation during hurricane season? If you’re traveling somewhere prone to cyclones, typhoons, or hurricanes, buying travel protection is wise. It can help you recover non-refundable costs and provide coverage for trip cancellation if you need it.

On the other hand, perhaps you decided traveling in a hurricane-prone region during hurricane season just isn’t worth the risk. That’s completely understandable. If that’s the case, then here are four destinations a hurricane will never hit.

Skylar, a seasoned content writer with over seven years of experience, possesses a deep understanding of the travel and travel insurance industries. Her commitment to authenticity infuses her work with a unique perspective, drawing from three years of dedicated writing in the travel and travel insurance sectors. Skylar's expertise is further enriched by her proactive approach to seeking insights from industry professionals, ensuring that her findings are comprehensive and reliable.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Departure Date Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Return Date Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

State of Residence Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Number of Travelers Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Trip Cost Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Deposit Date Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Travel Style Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

When Is Hurricane Season?

When Is Hurricane Season?

Enroll in STEP

Enroll in STEP Buy Travel Insurance As Soon As Possible

Buy Travel Insurance As Soon As Possible

Stay Flexible With Your Travel Activities

Stay Flexible With Your Travel Activities Determine The Stability Of Your Destination

Determine The Stability Of Your Destination Plan An Emergency Departure

Plan An Emergency Departure Pack Like A Hurricane Might Happen

Pack Like A Hurricane Might Happen