How Does Travel Insurance for Pre-Existing Conditions Work? (2026 Guide)

February 20, 2024 - Meagan Palmer

Last Updated On:

Traveling with a chronic illness or recent medical history can add an extra layer of planning to your trip. If you or someone you’re traveling with has a current health condition, understanding how travel insurance for pre‑existing conditions works can make a major difference in protecting your investment and your well‑being.

Quick Answer

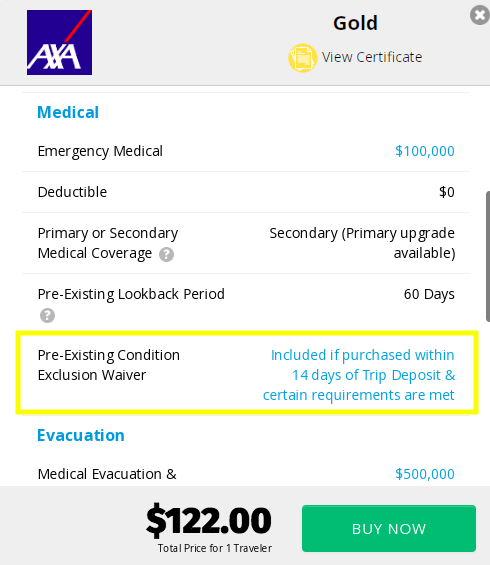

Yes, you can get travel insurance with a pre-existing condition. To ensure coverage for flare-ups, you typically need a Pre-Existing Condition Waiver. This waiver is usually only available if you purchase your policy within 14 days of your initial trip deposit and insure 100% of your non-refundable costs. Without a waiver, insurers use a “lookback period” (60–180 days) to determine if a condition is covered.

Key Takeaways

The “Lookback Period” is Critical: Travel insurers review your medical history from the 60 to 180 days before you purchase your policy to determine if a condition is “pre-existing.”

Waivers Provide Full Coverage: A Pre-Existing Condition Waiver is the only way to ensure that flare-ups or complications from an existing illness are covered during your trip.

Timing is Everything: To qualify for a waiver, you must typically purchase your policy within 14 days of making your initial trip deposit.

Insure 100% of Costs: Most waivers require you to insure all non-refundable trip expenses and be medically fit to travel on the day you buy the policy.

Stable Conditions May Not Need a Waiver: If your condition has been “stable” (no new symptoms or medication changes) throughout the entire lookback period, it may be covered as a standard medical event.

Non-Traveling Family Members: Their health history isn’t “pre-existing” to your policy, but a claim for their illness will only be approved if it was an unforeseen event (not a known health crisis) at the time of purchase.

What is the Definition of a Pre-Existing Condition in Travel Insurance?

Unlike standard health insurance, travel insurance uses a specific timeframe called a “Lookback Period.” This is typically the 60 to 180 days immediately preceding your policy’s effective date. During this time, a provider reviews your health history to establish any connection between your claim and something ongoing.

With travel insurance, a pre-existing condition is any ongoing condition or change in your medical history occurring in the last 60 to 180 days before your policy’s effective date.

A condition is considered pre-existing, if these kinds of events occurred within the lookback period:

A doctor recommends you take a medical test, examination, or medical treatment.

Your physician prescribed a new medication for you.

You experienced a change in dosage or frequency of your prescription.

Does travel insurance consider pregnancy a pre-existing condition?

In many policies, pregnancy and routine childbirth are excluded. However, specific complications of pregnancy may sometimes be covered depending on the policy. We have a full article discussing whether pregnancy is covered by travel insurance if you’d like more detail.

Even if you fall into one of the scenarios above, you may still be able to get coverage through a pre‑existing condition waiver, depending on when you buy your policy and whether you meet eligibility requirements. More on that later.

What’s NOT considered a pre-existing condition under travel insurance?

Fortunately, since providers typically review medical records only for the preceding three to six months, many long‑standing conditions fall outside the lookback window. The key is that your condition has remained stable recently for coverage to apply in relation to a flare-up.

For example, if you received a cancer diagnosis five years ago and have had no recent treatments, symptoms, or changes to your health records during the lookback period, the insurer may not treat it as a pre‑existing condition for the purposes of your policy.

Similarly, stable chronic conditions managed with long‑term medication often qualify for coverage. For instance, many travelers successfully obtain trip insurance while managing stable diabetes or blood pressure with medication, provided there were no recent adjustments.

What About Family Member’s Pre-Existing Conditions?

We often get asked about non-traveling family members who experience medical maladies. Because a non-traveling family member is not the policyholder, their health history is not technically categorized as a “pre-existing condition” for your plan. However, this does not mean all their medical issues are covered.

However, travel insurance is designed to protect against the unexpected. To determine if your claim is valid, providers look at two specific scenarios:

Known Events (Not Covered): If a non-traveling family member is currently experiencing a health crisis at the time you purchase your policy, any subsequent cancellation related to that specific event is typically excluded. Because the event was already in progress, it is no longer “unforeseen.”

Unforeseen Events (Covered): If a family member becomes unexpectedly ill, suffers an injury, or passes away after your policy has gone into effect, you have a much higher likelihood of your cancellation benefits kicking in.

Pro Tip: To ensure the best protection, purchase your travel insurance as soon as you make your first trip deposit. This “locks in” your coverage before any health issues at home can transition from “unforeseen” to “known.”

Pre-Existing Condition

NOT a Pre-Existing Condition

A recent change in your health history that could affect your trip

An illness or injury that has fully resolved

An ongoing medical condition that requires regular treatment or monitoring

An ongoing medical issue stabilized via medication or hasn’t required continued treatment

A new medical diagnosis within the policy lookback period

A new medical condition that arises after the policy effective date

What value does a travel insurance pre-existing condition waiver offer?

A pre‑existing condition waiver removes the usual exclusion that travel insurance applies to existing medical issues. Without the waiver, travel insurance will typically reimburse trips disrupted only by new medical events. If your existing condition worsens and prevents travel, the claim may not be covered.

For travelers with ongoing conditions, having trip protection that covers potential flare‑ups provides real peace of mind,” says Terry Boynton, co-founder and president of Yonder Travel Insurance.

This coverage is particularly helpful since most travelers’ domestic health insurance or Medicare provides limited coverage outside the United States. International emergency treatment and evacuations can be extremely costly without travel insurance.

Some policies automatically include pre-existing condition waivers, but it’s important to check the requirements to ensure eligibility for coverage.

Common Requirements Include:

Purchasing the policy within a specific timeframe (usually within 14 days of your initial deposit).

Insuring all nonrefundable trip costs

Being medically able to travel at the time the plan is purchased

Buying travel insurance early is important. If you miss the waiver window, you may still buy a policy, but claims related to the condition may be excluded.

Even if you’ve missed the 14-day purchase window, there might be a few plans that extend eligibility if you purchase coverage before or within about 24 hours of making your final trip payment.

What Coverage Pre-Existing Condition Waivers Apply To

If you have a pre-existing medical condition, several parts of your trip could potentially be affected.

A flare‑up may force you to cancel your trip before departure, interrupt your trip, or require medical care while traveling.

Policies with a waiver may activate these benefits:

Trip Cancellation/Trip InterruptionExample

A traveler with a heart condition purchases travel insurance with a pre‑existing condition waiver. Their doctor later advises them not to travel just before departure due to worsening symptoms. The policy could reimburse prepaid trip costs.

Medical Expense/Medical Evacuation Example

If a traveler with heart disease requires emergency treatment abroad or needs evacuation to a larger hospital, the waiver allows the policy to cover those costs related to the ongoing condition.

These protections can be particularly valuable on cruises or international trips where medical evacuation costs can reach $50,000 or more.

Recap of Why You May or May Not Need a Pre-Existing Condition Waiver

In short, if recent health changes concern you regarding your trip, consider purchasing a pre-existing condition waiver with your travel insurance.

Travelers often choose policies with this benefit when:

They’re recovering from surgery and want reassurance in case recovery takes longer

A recent diagnosis could potentially affect travel plans

Their doctor cleared them to travel but recommended to take precautions before their trip

They want coverage if symptoms worsen before departure

Pro Tip: If your condition has been stable for months or years without recent treatment changes, you may not need a waiver, but confirming the policy lookback period is always wise.

Eligibility Checklist: Do I Need a Pre-Existing Condition Waiver?

Did you have a change in medication in the last 180 days?

Have you seen a doctor for a new symptom recently?

Is your condition “unstable” (recent flare-ups)?

Result: If you answered “yes” to any of the above, you likely require a Pre-Existing Condition Waiver to have medical coverage for that specific condition during your trip.

How to Purchase Travel Insurance for Pre-Existing Conditions

Luckily, it’s simple to get coverage for ongoing medical conditions if you already qualify.

Get a Quote Early: Start your search within 14 days of your first trip payment to ensure the widest selection of waiver-eligible plans.

Use the “Waiver” Filter: On the Yonder Quote Tool, select the filter for “Pre‑Existing Condition Waiver” to hide plans that won’t cover your medical history.

Insure 100% of Costs: To qualify for a waiver, most insurers require you to insure the full, non-refundable value of your trip.

Confirm the “Lookback Period”: Check if the plan uses a 60, 90, or 180-day window. A shorter window is better if you had a health change several months ago.

If questions come up, Yonder’s licensed insurance experts can help explain policy details and eligibility requirements.

For additional guidance, visit our Travel Insurance FAQ page, which answers many common travel insurance questions.

How to Compare Travel Insurance PoliciesThat Include Pre-Existing Condition Coverage

Choosing the best travel insurance for chronic conditions involves more than just price. A careful comparison helps ensure coverage actually applies when you need it.

Here are a few tips our experts at Yonder Travel Insurance adhere to.

1. Check the Lookback Period

The lookback period determines how far back insurers review medical history, typically 60 to 180 days. A shorter lookback period may mean fewer conditions qualify as pre‑existing.

2. Confirm Waiver Eligibility Deadlines

Many travelers miss coverage simply by waiting too long to buy insurance. Try getting your coverage within the first two weeks (or sooner!) to have a wider selection of plans that include travel insurance for pre-existing condition.

Travel Insurance for Pre-Existing Conditions FAQ

Does travel insurance cover pregnancy as a pre-existing condition?

Normal pregnancy is usually not covered by standard travel insurance. However, some policies do provide benefits if certain pregnancy complications arise. For full details, read our guide to pregnancy travel insurance.

Can I still get a pre-existing condition waiver if I missed the 14-day window?

Since most plans with this coverage have to be purchased within this timeframe from your deposit date, it’s less likely. However, some providers allow pre-existing condition coverage if you haven’t yet paid for your final trip payments.

What happens if I don’t get a pre-existing condition waiver?

If you forgo or can’t get a waiver, your policy still covers new illnesses or injuries. However, if you file a claim related to an existing condition, the insurer will perform a “medical lookback.” If your medical records show any changes or treatments for that condition within the 60–180 days before you bought the policy, the claim will likely be denied.

Meagan has spent over seven years at Yonder Travel Insurance mastering the "fine print" so travelers don’t have to. With a background spanning marketing and operations, she specializes in deconstructing complex policy jargon into clear, actionable advice that empowers travelers to explore with confidence. From selecting the perfect plan for a niche itinerary to navigating the intricacies of the claims process, Meagan provides the unbiased, expert travel insurance insights necessary to maximize benefits and minimize risk. By maintaining close partnerships with the travel insurance industry’s top providers, she stays at the forefront of emerging trends, ensuring her readers are always one step ahead of the unexpected.

Get an instant travel insurance quote!

Step 1

Step 2

Step 3

Destination

Where are you going?

If you're traveling to multiple countries, select the country you're spending the most time in.

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Departure Date Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Return Date Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

State of Residence Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Number of Travelers Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Trip Cost Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Deposit Date Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

Travel Style Info

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur. Excepteur sint occaecat cupidatat non proident, sunt in culpa qui officia deserunt mollit anim id est laborum

What is the Definition of a Pre-Existing Condition in Travel Insurance?

What is the Definition of a Pre-Existing Condition in Travel Insurance?